Keep Your Home Safe During the Busiest Time of Year The holiday season is one…

This Is How A Cross Collateralization Loan Works (Buy A Property Using Existing Equity)

In this guide, you’ll learn what a cross collateralization loan is, how it works, who it’s for, its requirements, the risks involved, and a clear example showing how the numbers work.

What Is a Cross Collateralization Loan?

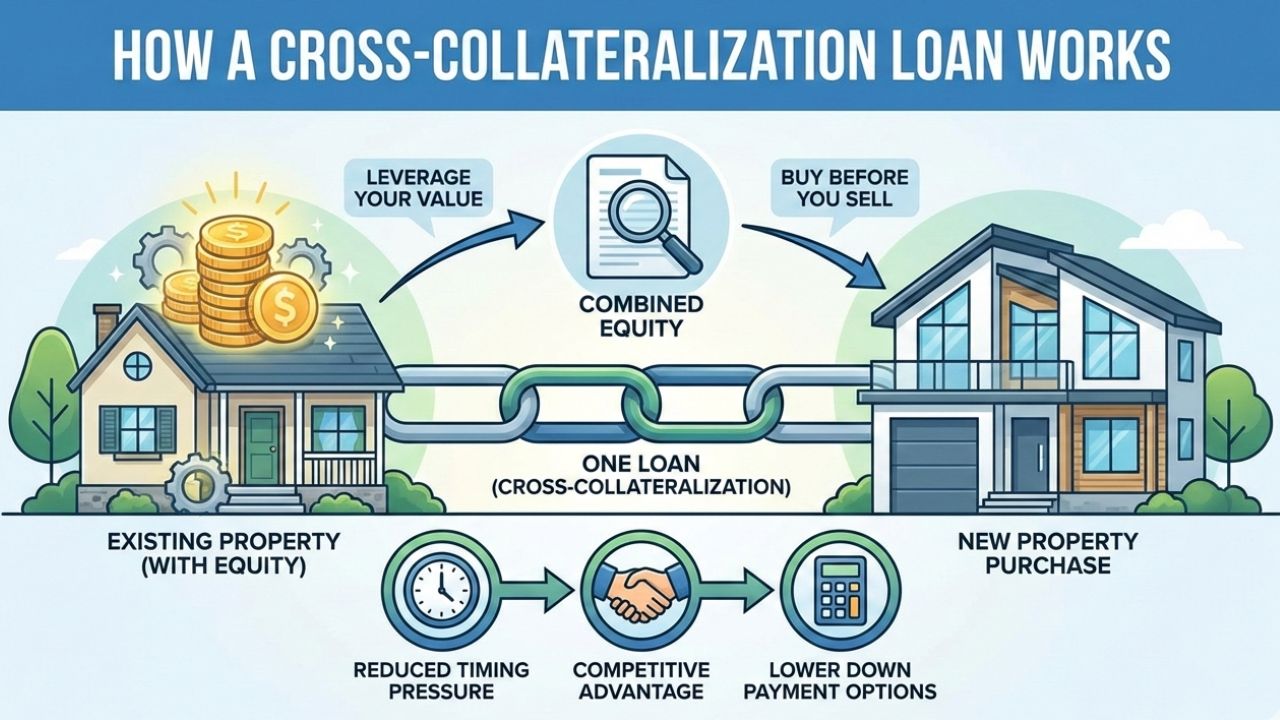

A cross collateralization loan is a financing strategy where a lender uses more than one property as collateral for a single loan. Instead of selling your current property to fund a new purchase, you temporarily tie both properties together under one loan.

This approach is most commonly used in strong seller’s markets, where buying before selling gives you a competitive advantage. It allows you to leverage existing equity rather than rushing into a sale or taking out a high-cost bridge loan.

Why Investors and Homebuyers Use Cross Collateralization

When you want to buy a new property before selling your current one, your options are limited. Bridge loans can be expensive, and simultaneous buy-sell transactions can be stressful and risky.

A cross-collateralization loan simplifies the process by creating a single temporary loan secured by multiple properties. This reduces timing pressure, lowers stress, and often costs less than short-term hard money solutions.

How Cross Collateralization Works

You use the equity from your existing property, or multiple properties, as additional collateral for the new purchase. The lender evaluates the combined value of the properties rather than each one individually.

This makes it possible to:

- Buy before you sell

- Reduce or eliminate a down payment

- Access higher loan amounts

- Avoid temporary bridge financing

Once your original property sells, you typically refinance into a standard loan and release the cross collateralization.

Requirements for a Cross Collateralization Loan

Cross collateralization loans are designed for larger transactions and have specific requirements.

The loan must be a purchase loan, not a refinance. It can be used for primary residences, second homes, or investment properties. These loans are adjustable-rate only, as they are intended for short-term use.

You generally need a minimum credit score of 680. Loan amounts typically start at around $500,000 and can reach $5 million or more, depending on the lender.

Lenders also require at least six months of reserves. Reserves are calculated using your monthly principal, interest, taxes, and insurance payment multiplied by the required number of months. These reserves need not be in cash and can include retirement accounts and other liquid assets.

Most cross collateralization loans include a prepayment penalty. Many borrowers offset this penalty by accepting a slightly higher interest rate, allowing them to refinance or sell later without penalty concerns.

Cross Collateralization Loan Calculation

The calculation follows a straightforward formula.

First, add the market value of your existing property and the new property you want to buy. Then multiply that total by 60 percent. From that number, subtract any existing loan balances on your current property. The result is the maximum loan amount you can borrow.

This final number determines how much you need to put down on the new purchase. In some cases, the down payment can be very small or even zero, depending on equity levels.

Example of a Cross Collateralization Loan

Assume your current property is valued at $2 million with an existing loan balance of $500,000. You want to buy a new property valued at $3 million.

You combine the values to get $5 million. Sixty percent of that is $3 million. After subtracting the $500,000 existing loan, your available loan amount becomes $2.5 million.

This means you can borrow $2.5 million toward the new purchase and only need to bring the remaining amount as a down payment. In this example, the loan-to-value ratio reaches approximately 83 percent, which is difficult to achieve with standard jumbo financing.

Do You Still Need to Qualify?

Yes. Even though you are using equity, you still must qualify based on income, debt-to-income ratios, credit history, and reserves. Cross collateralization helps with structure, not qualification. If you meet the financial requirements, this strategy can be a powerful way to move forward without waiting for a sale.

When a Cross Collateralization Loan Makes Sense

This type of loan works best if you

- Have significant equity,

- Are buying in a competitive market,

- Plan to sell or refinance within a relatively short period.

Final Thoughts

A cross collateralization loan can be a smart solution when timing matters and equity is available. It offers flexibility, reduces pressure, and opens doors that traditional financing often cannot. If used correctly, it can help you secure your next property while maintaining control over your existing assets.

Related Posts