For many first-time homebuyers or those with less-than-perfect credit, navigating the world of mortgage options…

FHA 3-4 Unit Property Self-Sufficiency Test Explained

If you’re considering buying an FHA 3-4 unit property, it’s important to understand the self-sufficiency test. This test is a key requirement for multi-unit properties when using an FHA loan. In this blog post, we’ll break down the process, the importance of the self-sufficiency test, and what you can do if your property doesn’t pass.

FHA 3-4 Unit Property Self-Sufficiency Test Explained

Buying a 3-4 unit property with an FHA loan is an excellent way to start your real estate investment journey, especially if you’re looking to generate income from the additional units. However, before you proceed, take the self-sufficiency test, which is required for FHA loans on multi-unit properties. Essentially, the property must be able to support the mortgage payments with rental income from the other units, ensuring your investment is financially viable.

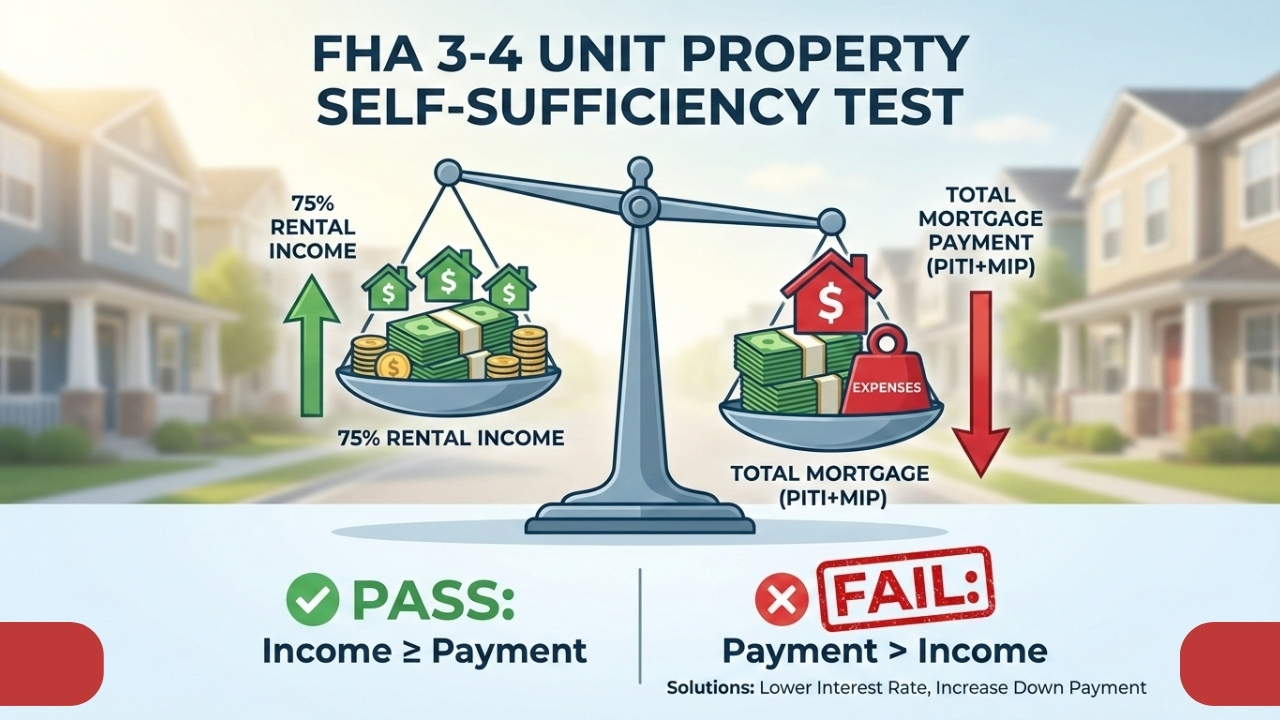

What Is the Self-Sufficiency Test?

The FHA guidelines state that for a property to pass the self-sufficiency test, the rental income must cover at least 75% of the total mortgage payment. This includes principal, interest, taxes, insurance, and mortgage insurance premiums. If the property doesn’t meet this requirement, you might not qualify for the loan.

A Case Study: FHA 3-4 Unit Property in Chicago

Let’s dive into an example of a three-unit property in Chicago. The purchase price for this property is $450,000, and each unit rents for $1,600 per month, giving a total rental income of $4,800. However, the total monthly mortgage payment, including all expenses, is $4,818.

By applying the self-sufficiency test, we take 75% of the total rental income, which is $3,600. Since $3,600 is less than the mortgage payment of $4,818, this property doesn’t pass the FHA self-sufficiency test. As a result, the buyer would not qualify for an FHA loan under these conditions.

Why the Self-Sufficiency Test Matters

The self-sufficiency test is designed to ensure that the property can financially sustain itself. While the idea of renting out a portion of your property to cover your mortgage is appealing, the reality is that rental income doesn’t always fully cover the costs. Without passing the self-sufficiency test, you may need to explore other options to make the property financially viable.

Solutions for Success

If you find that your property doesn’t pass the self-sufficiency test, there are a few potential solutions:

- Lower the Interest Rate – A lower interest rate can help reduce the monthly payment, making it easier for rental income to cover a larger portion of the mortgage. You can achieve this by negotiating a seller credit to buy down the interest rate.

- Increase the Down Payment – By putting more money down, you reduce the loan amount, which can lower the monthly mortgage payment. This can help meet the 75% threshold for the self-sufficiency test.

- Combine Both Solutions – You can also combine both strategies—lower the interest rate and increase the down payment—to ensure the property passes the test.

Although these solutions require some extra effort, they could make the difference between qualifying for an FHA loan or not. It’s important to remember that the self-sufficiency test is just one of many factors that affect your ability to purchase a multi-unit property with an FHA loan. Always work with a knowledgeable mortgage advisor to find the best solution for your situation.

Final Thoughts

The self-sufficiency test is a crucial component when buying an FHA 3-4 unit property. By understanding how it works and identifying potential solutions, you can ensure your investment is financially sound. Remember, the goal is to ensure your rental income covers the majority of the mortgage payment, so always consider all your options before moving forward.

Related Posts