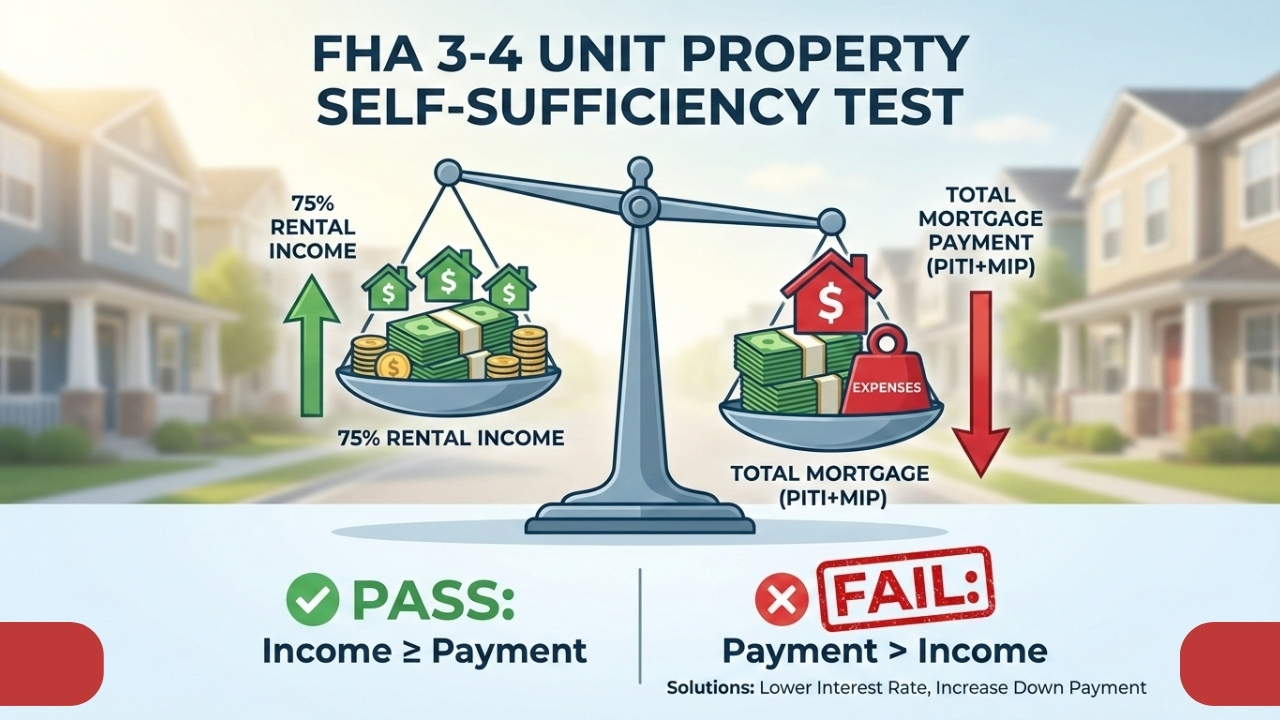

If you're considering buying an FHA 3-4 unit property, it's important to understand the self-sufficiency…

How to Get a DSCR Loan on Long-Term Rental Properties

In this blog post, we’ll walk through a detailed case study on how to get a DSCR loan on long-term rental properties. We break down the entire process, from understanding the loan’s financial requirements to calculating closing costs, cash flow, and reserves. Using a real example, we show you how to make this type of loan work for your property investment and demonstrate precisely what you need to consider before applying.

DSCR Loans: What You Need to Know

A DSCR loan allows you to qualify for a mortgage based on the rental income generated by your property. This makes it ideal for investors without a traditional income source. In this case study, we explore a three-unit property in Chicago listed for $450,000. The rental income per unit is $1,600, for a total of $4,800 per month. With a 25% down payment ($112,500), the loan amount would be $337,500, with an 8.5% interest rate.

Once you factor in the monthly principal, interest, taxes, and insurance payment of $3,463, we can calculate the DSCR ratio. The rental income ($4,800) exceeds the loan payment ($3,463), resulting in a DSCR of 1.39 and indicating positive cash flow. This property would generate a monthly cash flow of $1,337—an excellent return for an investor.

Closing Costs and Cash to Close

When you’re applying for a DSCR loan, you’ll encounter additional costs like discount points, lender fees, title and escrow fees, and prepaids. In this example, the total closing cost estimate is $15,937. Combined with the $112,500 down payment, the total cash to close would be $28,495.

Reserves: What You Need to Have

In addition to the down payment and closing costs, DSCR loans typically require reserves. These reserves, which are not part of the transaction itself, must be liquid and available in case of an emergency. For a DSCR loan, you’ll generally need reserves equivalent to 3-6 months of the loan payment. In this case study, the reserve requirement is calculated at $20,778.

Is a DSCR Loan Right for You?

In summary, getting a DSCR loan for long-term rental properties is a great option for real estate investors who need financing based on property income. You can estimate your cash flow, calculate your closing costs, and account for reserves to ensure you’re ready for a successful property investment. If you’re ready to apply for a DSCR loan, consider reaching out to a mortgage professional to guide you through the process.

Related Posts